With the Dec. 15 insurance enrollment deadline approaching, many people are already facing steep increases in premium prices. With the expiration of extensions to the Affordable Care Act (ACA) Premium Tax Credits (PTCs), millions enrolled in Marketplace plans will see their health insurance premiums rise–and in many cases, more than double.

What Does the ACA Do?

The ACA, signed into law in March 2010, aimed to do three things:

Expand Medicaid to include higher-income earners who still struggle to afford health insurance and previously didn’t qualify

Create health care marketplaces where individuals and small businesses can choose insurance plans and receive financial assistance through cost-sharing and PTCs

Require large employers to pay penalties when they do not provide affordable coverage to employees

How Do Premium Tax Credits Work?

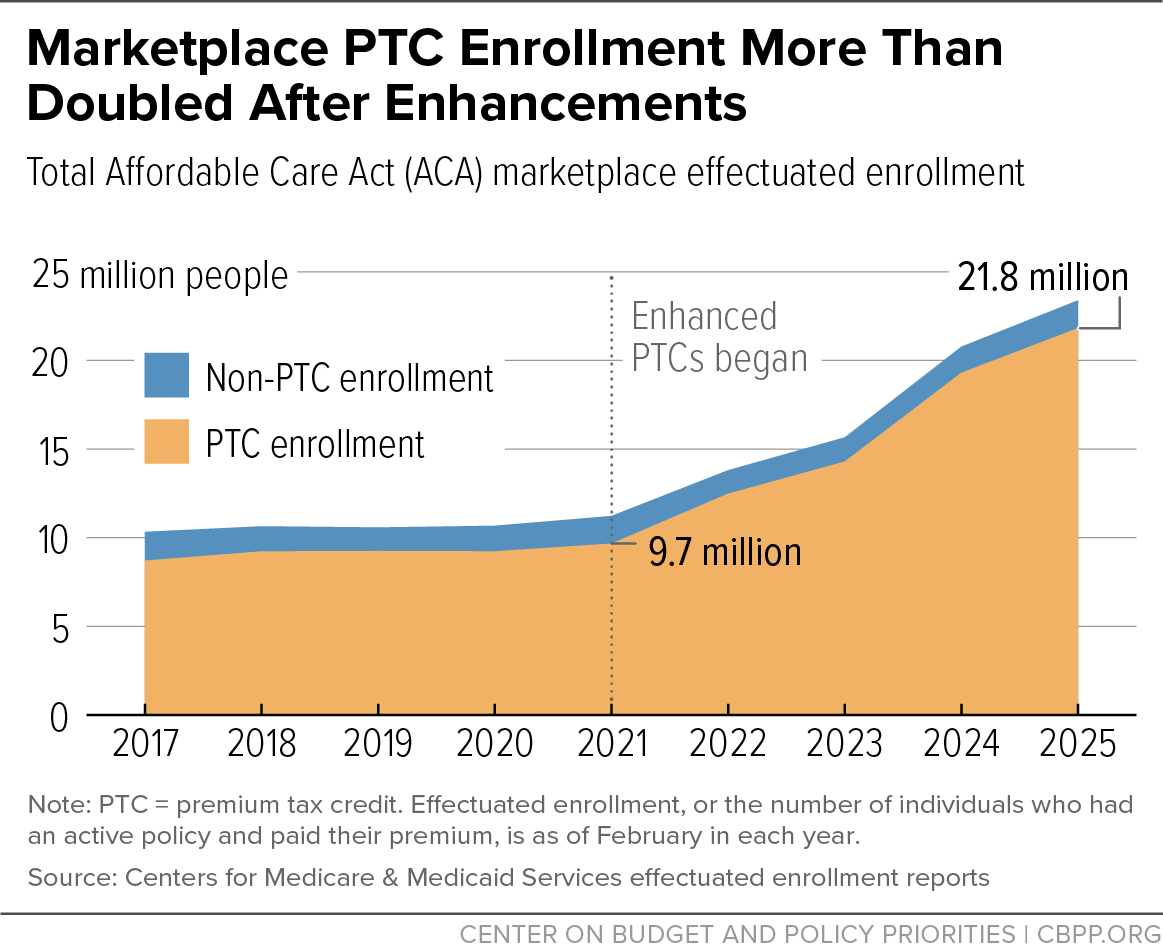

PTCs are refundable tax credits that help eligible individuals purchase subsidized health care plans on the marketplace. Insurance premiums are quoted based on a sliding scale–PTCs then cover the difference between what the individual is expected to contribute and the actual cost of the plan. That contribution is set by the family’s income–so lower earners pay less than higher earners. During the COVID-19 pandemic, Congress passed the American Rescue Plan Act (ARPA) of 2021, which expanded eligibility for higher-income earners and reduced contributions for families across all income levels. This expansion increased access to health care for millions of people who were struggling to afford insurance.

Example 1: John is a 24-year-old making $30,120 per year. His expected contribution is 2% of his income, or $602. The plan available to him costs $5,000 per year. His tax credit would cover $4,398.

Example 2: Peter, Mary, and their two children have an annual income of $78,000, with an expected contribution of 4% ($3,120). The plan available to the family costs $15,000. With PTCs, their tax credit would cover $11,880.

How Did PTCs Play Into the Government Shutdown?

The expansion to PTCs under ARPA is set to expire at the end of fiscal year 2025. When that happens, premiums for 20 million Americans will increase beginning in January 2026. Many elected officials have advocated for extending PTCs permanently. However, a lack of agreement led Congress to fail to pass a funding bill before Oct. 1, 2025, resulting in the government shutdown.

What Can We Expect?

By 2025, enrollment through ACA marketplaces totaled around 23.4 million people—double the amount in 2020, totaling 11.4 million. This indicated a growing need for health insurance subsidies as more people rely on Premium Tax Credits (PTCs) to afford health care. Specifically, low-income people make up the vast majority of growth in the ACA marketplaces, further highlighting the unaffordability of health care.

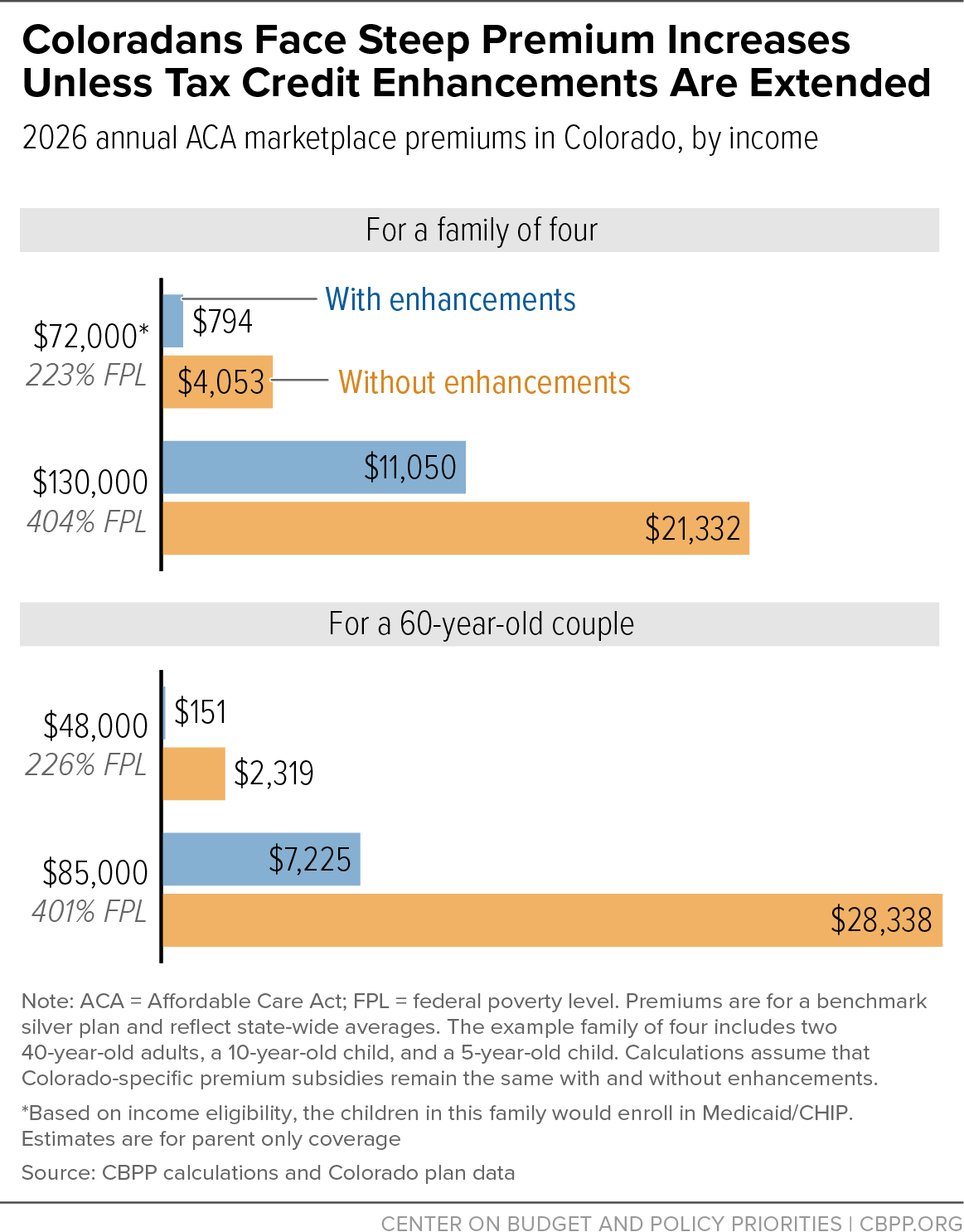

With the end of the extension to Premium Tax Credits (PTCs), premiums will increase for most of these individuals and their families. Without these subsidies, premium costs would double or more than double for many. Subsequently, lower-income enrollees would see the steepest premium increase. For example, a 45-year-old enrollee making $25,000, currently paying $160 for their annual premium, would now be paying up to $1,077 per year without the subsidy—a 573% increase.

With higher premiums, more people will opt out of coverage. An estimated 3.8 million fewer people will have health care due to its unaffordability. As more people become uninsured, it increases the risk for those who are reliant on health care, as it increases premium costs for people without subsidies. When there are fewer people reliant on a service—in this case health insurance—the price goes up, making it more expensive for people who rely on services.

As services are still needed, state and local governments will likely see a strain as many uninsured require medical care—placing a strain on hospitals’ budgets, which must cover the unaccounted-for care.

People will get sick and use medical services regardless of whether they have insurance. What changes is when and where they seek care: uninsured people often delay treatment until their conditions worsen, and then they go to emergency rooms. Because preventive care isn’t accessible to the uninsured, they are often sicker when they seek care and generate higher uncompensated care costs for hospitals, straining their budgets. State and local government then absorb much of this burden through public hospital funding. In this way, the loss of insurance triggers a domino effect that impacts not only the individual but also providers, hospitals and government budgets.

So What Now?

These changes to health care subsidies could leave millions uninsured, stripping people of access to basic care and treatment. It is crucial to advocate for an extension of PTCs, as they remain a vital bridge to affordable and accessible health care. With a re-vote on PTC extensions approaching, contact your local legislators and urge them to support policies that keep health care accessible and affordable for the people they serve. Stay connected with the Colorado Fiscal Institute’s resources and join us in advancing people-centered policy.

By Shana McClain Most people probably never think about Medicaid renewals until a letter shows up reminding them of the cumbersome task. Now, however, H.R. 1 changes how often that…

Impacts on Essential State and Federal Programs Colorado’s immigrant communities are facing significant challenges as recent federal policy changes threaten access to essential programs and services. H.R. 1, signed by…

Gov. Jared Polis released his recommendations for Colorado’s 2026-27 state budget on Oct. 31, outlining another difficult year ahead for lawmakers. The proposal sets the stage for the Joint Budget…

Desde reformas fiscales hasta actualizaciones presupuestarias, desglosamos cuestiones complejas para mantenerle informado sobre las decisiones políticas que afectan a nuestras comunidades.

Este sitio web utiliza cookies para mejorar su experiencia. Algunas son esenciales para el funcionamiento del sitio, mientras que otras nos ayudan a analizar y mejorar su experiencia de uso. Revise sus opciones y haga su elección.

Si tiene menos de 16 años, asegúrese de haber recibido el consentimiento de su padre o tutor para todas las cookies no esenciales.

Su privacidad es importante para nosotros. Puede ajustar sus configuraciones de cookies en cualquier momento. Para obtener más información sobre cómo utilizamos los datos, lea nuestra política de privacidad. Puede cambiar sus preferencias en cualquier momento haciendo clic en el botón de configuraciones a continuación.

Tenga en cuenta que, si elige desactivar algunos tipos de cookies, esto puede afectar su experiencia en el sitio y los servicios que podemos ofrecer.

Las cookies y servicios esenciales habilitan funciones básicas y son necesarias para el correcto funcionamiento del sitio web. Estas cookies y servicios no requieren el consentimiento del usuario según el RGPD.

Las cookies de estadísticas recopilan información de uso, lo que nos permite obtener información sobre cómo interactúan los visitantes con nuestro sitio web.

Los servicios de marketing son utilizados por anunciantes o editores terceros para mostrar anuncios personalizados. Hacen esto al rastrear a los visitantes en múltiples sitios web.

Esta categoría incluye todas las cookies, dominios y servicios que no se incluyen en las otras categorías específicas o que no han sido categorizadas explícitamente.

Este sitio web utiliza cookies para mejorar su experiencia de navegación y asegurar el correcto funcionamiento del sitio. Al continuar utilizando este sitio, reconoce y acepta el uso de cookies.